AI Finance · Venture Capital · Q1 2026 · April 17, 2026

The total global venture capital invested in all of 2023 — across every sector, every country, every stage — was approximately $285 billion. In the first quarter of 2026, AI companies alone raised $242 billion. In three months. In one sector. This is what a genuine paradigm shift looks like in the capital markets.

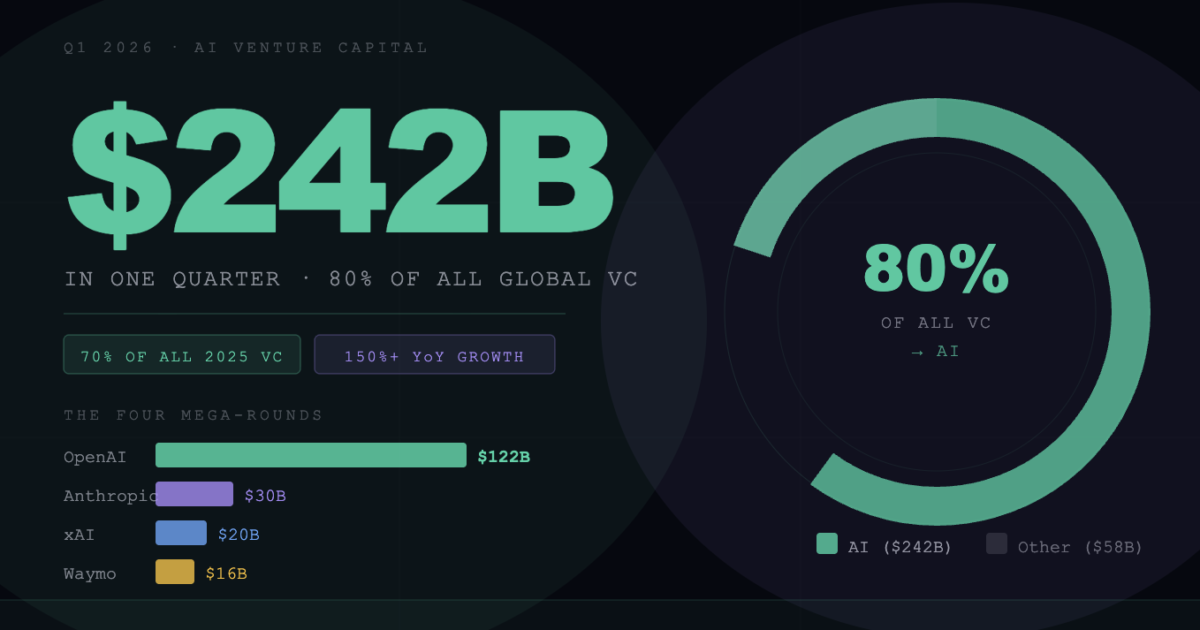

According to Crunchbase data, global venture investment reached $300 billion in Q1 2026 across roughly 6,000 startups. That single quarter absorbed close to 70% of all global venture capital deployed in the entirety of 2025. Year-on-year growth exceeded 150%. And 80% of it — $242 billion — went to AI.

Four Deals That Defined a Quarter

Four of the five largest venture rounds ever recorded in history were closed in a single quarter. Together they account for $188 billion — nearly 65% of all global venture capital in the period.

The Four Mega-Rounds — Q1 2026

- OpenAI — $122 billion: The largest private fundraise in history. Led by Amazon, NVIDIA, and SoftBank. OpenAI now generates $2B+ in monthly revenue and is targeting an IPO in late 2026.

- Anthropic — $30 billion: Series G at a $380 billion post-money valuation. Total capital raised now exceeds $64 billion since founding in 2021.

- xAI (Elon Musk) — $20 billion: Series E. Positions xAI as a genuine third-force frontier lab. Grok ranks second globally on Arena Elo ratings as of April 2026.

- Waymo — $16 billion: Series D. The autonomous vehicle company now operates approximately 450,000 weekly paid trips across five US cities. Physical AI is reaching commercial scale.

Putting $242 Billion in Context

Scale Reference Points

- Total global VC in all of 2023 across every sector: ~$285 billion. AI alone raised $242B in Q1 2026.

- Q1 2026 represents nearly 70% of all global venture capital deployed in the entirety of 2025.

- The Q1 total exceeds every full-year investment total prior to 2018.

- Year-on-year growth: more than 150%.

- AI’s share of global VC: from 55% in Q1 2025 to 80% in Q1 2026 — a 25-point swing in one year.

- US companies captured $250 billion — 83% of global VC, up from 71% a year earlier.

Where the Money Went

| Category | Q1 2026 Investment | Signal |

|---|---|---|

| Frontier AI labs (model builders) | $178B+ | Doubled the $88.9B raised across all of 2025 |

| Autonomous vehicles / physical AI | $20B+ | Physical AI reaching commercial deployment scale |

| AI application layer (B2B) | $25.1B (Series A/B) | Up 56% YoY — strongest early-stage showing in 3 years |

| Non-AI startups | ~$58B | Competing in a secondary capital tier |

The Early Stage Reality — A Tale of Two Markets

Early-stage funding grew: $41.3 billion at Series A and B, up 41% year-on-year, and seed funding reached $12 billion, up 31%. But the number of seed deals actually fell by around 30%, meaning fewer companies are receiving larger cheques. Deal count dropped 26% in North America even as dollars invested surged 190%.

“When 80% of all global venture capital flows to one sector in a quarter, founders building outside it aren’t competing on a level field. They are competing in a secondary capital tier.”

— TechRound Analysis, April 2026The Q1 2026 record was not a rising tide that lifted all boats. It was a flood concentrated in a very small number of very large vessels, while the broader market remained uncertain.

The Geographic Concentration Problem

The United States captured $250 billion — 83% of global VC, up from 71% a year earlier. China was second at $16.1 billion. The UK came third at just $7.4 billion, representing 2.5% of the total. The funding distribution in Q1 2026 does not reflect the global distribution of talent or innovation. It reflects the gravitational pull of a handful of American AI frontier labs.

Is This a Bubble? The Honest Answer

The word “bubble” gets thrown around loosely. What the Q1 2026 data shows clearly: sky-high private valuations with no public market accountability, massive capital intensity in a small number of companies, and a disconnected IPO market that saw only 21 venture-backed companies exit above $1 billion globally in the quarter.

What it doesn’t show: that the underlying technology is valueless. OpenAI generates $2B+ monthly. Anthropic has $19B in annualised revenue. MIT Sloan experts draw parallels to the dot-com era, but the critical difference from 2000 is that the revenue is real. The honest answer: fundamentals are genuine, valuations are extrapolations, and capital concentration creates systemic risk if sentiment shifts before IPO markets open.

What $242 Billion Actually Means

For AI startup founders: Enterprise AI is where startups can win — enterprises need customisation, compliance, and integration that large labs don’t prioritise. Build proprietary data advantages. Use open-source models (Llama, DeepSeek, Qwen) to reduce API dependency and improve margins.

For enterprise buyers: Evaluate vendors on durability, not just features. A startup that raised at a $2 billion valuation in Q1 2026 on three months of revenue may not exist in 2028. Prioritise data privacy commitments and viable business models.

For everyone watching: The infrastructure constraint is real. A Bloomberg report found roughly half of US AI data centres planned for 2026 have been delayed or cancelled due to transformer shortages, grid strain, and supply chain bottlenecks. Only about one-third of projected new compute capacity is under active construction. The capital is there. The physical infrastructure to deploy it is not — yet.

The Verdict

$242 billion in one quarter is a declaration by the people who allocate capital professionally that they believe AI will restructure every major industry — and that the window to own foundational positions in that restructuring is now, not later. Whether they are right about the valuations, the question is not whether AI will transform the economy. It’s whether the private market prices of Q1 2026 will still look reasonable when these companies finally face public market scrutiny.

FAQ

How much did AI raise in Q1 2026?

AI companies raised approximately $242 billion in venture capital during Q1 2026, representing roughly 80% of all global startup investment in the quarter. Total global venture investment reached $300 billion — the highest quarterly total ever recorded.

Which companies raised the most in Q1 2026?

OpenAI raised $122 billion (the largest private fundraise in history), Anthropic raised $30 billion, xAI raised $20 billion, and Waymo raised $16 billion. Together these four deals accounted for $188 billion — approximately 65% of all global venture capital in the quarter.

Is the AI investment boom a bubble?

Nuanced. The underlying revenue is real — OpenAI generates $2B+ monthly, Anthropic has $19B annualised. But valuations are extrapolations and capital concentration creates systemic risk. There are structural similarities to the dot-com era, but with meaningfully stronger revenue fundamentals than 2000.

What is slowing down AI’s growth despite the record investment?

Physical infrastructure constraints. Roughly half of US AI data centres planned for 2026 have been delayed or cancelled due to transformer shortages, grid strain, and supply chain bottlenecks. Capital is available — physical infrastructure is the binding constraint.

Which country received the most AI investment in Q1 2026?

The United States dominated with $250 billion — 83% of global venture capital, up from 71% a year earlier. China was second at $16.1 billion. The UK came third at $7.4 billion, just 2.5% of the total.

Sources: Crunchbase Q1 2026 Global Venture Report, TechRound, PYMNTS, Benzinga, GrantedAI, Bloomberg, MIT Sloan Management Review · April 17, 2026 · clusters.media